Our data shows 14% fewer buyers in the market over the last 4 weeks than the average over the last 5 years. However, those that remain appear committed to moving home. This is evidenced by sales agreed running 8% above average, although with wide regional variations in the underlying supply/demand balance.

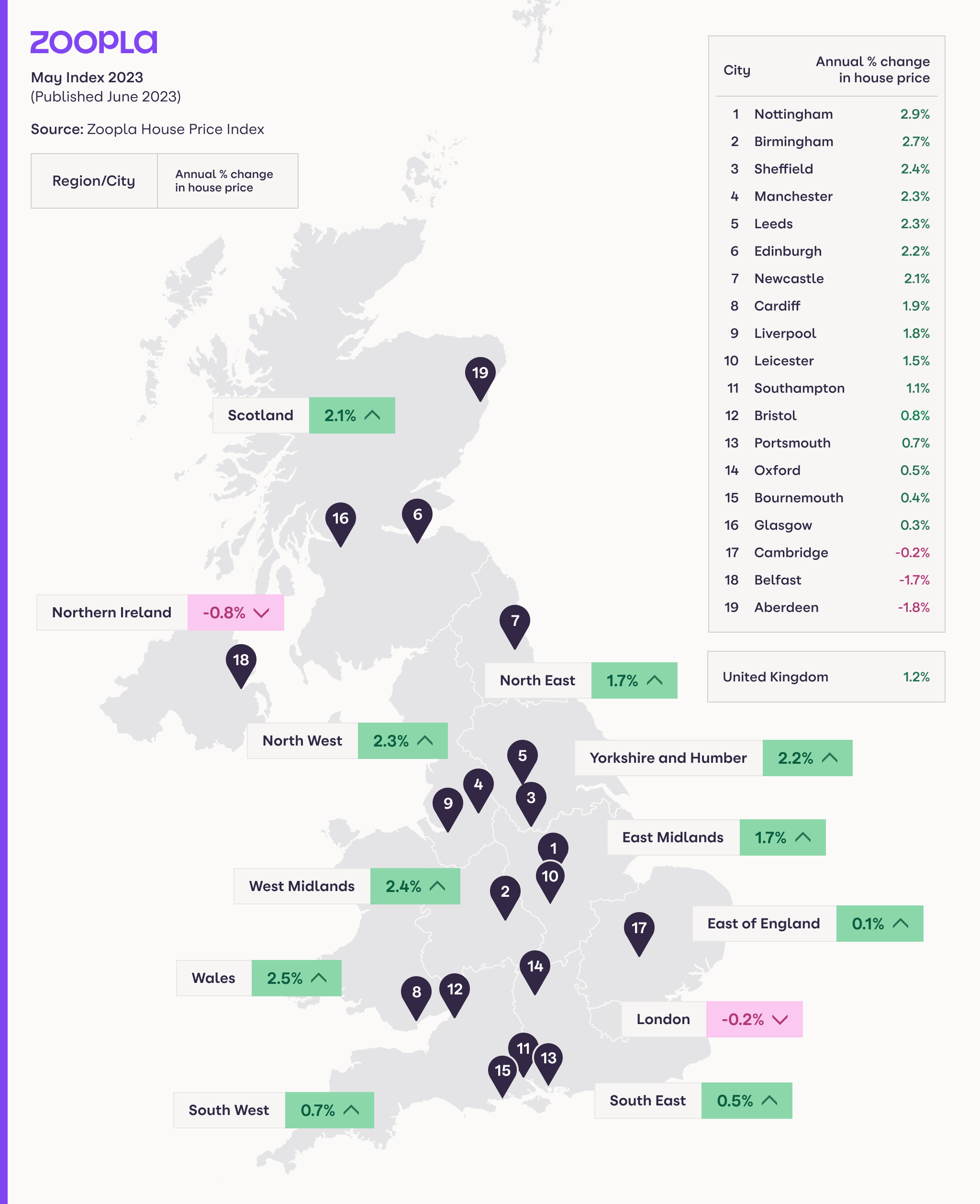

The number of new sales being agreed continues to run above the national average in Scotland, the North East, where housing is more affordable, and in London where price rises have under-performed.

Sales volumes remain at or below average in most English regions where house prices registered some of the greatest gains over the pandemic years. This has made homes less affordable, exposing sales volumes to the impact of higher mortgage rates on buying power.

Our localised house price indices show a clear link between price growth and the level of actual house prices. It’s markets with average prices over £350,00 where further price falls are most likely. The East of England, South-West, East Midlands and South-East are areas where it appears house prices will need to adjust the most.